California Drivers Are Re-Learning a Painful Lesson: Minimum Coverage Isn’t “Enough”

For years, plenty of California drivers treated auto insurance like a box to check: buy the cheapest policy that meets the minimum, keep the monthly payment low, and move on. But lately, more people are realizing how quickly that approach can backfire.

With higher repair costs, rising medical bills, and too many underinsured drivers on the road, “minimum coverage” is starting to look less like a safety net and more like a gamble. And the harsh truth often only shows up after a crash.

These limits can still be overwhelmed by modern repair and medical costs. According to state requirements outlined by the California DMV, minimum coverage is designed to meet legal standards—not necessarily financial protection.

What “Minimum Coverage” Really Means in California

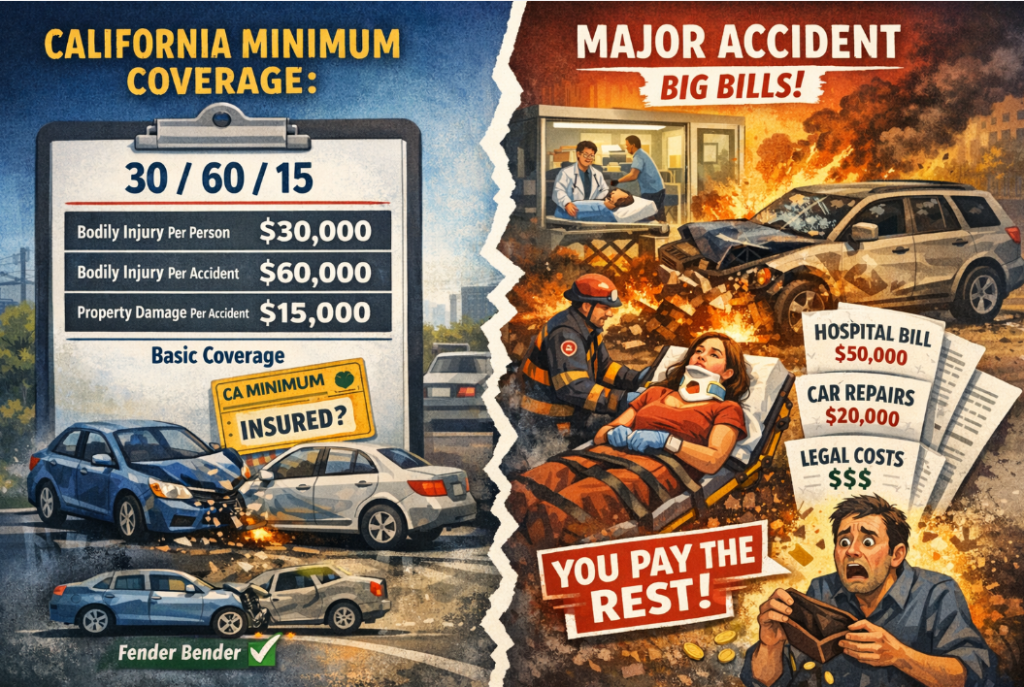

California requires drivers to carry liability insurance, but those minimum limits are exactly that: minimums. They’re designed to satisfy the law—not necessarily to protect your finances on a bad day.

In a minor fender bender, minimum limits might be enough. But accidents rarely stay “minor” for long. One emergency room visit, multiple injured passengers, or a newer vehicle packed with sensors and cameras can push costs past low limits surprisingly fast. When that happens, the remaining costs don’t disappear—they can land on you.

That’s why drivers often feel blindsided after an accident. They assumed “insured” meant “fully covered,” when in reality it meant “covered up to a low ceiling.”

California Minimum Limits at a Glance

| Coverage Type | Minimum Limit | What It Helps Pay For |

| Bodily Injury (per person) | $30,000 | Injuries or death to one person you harm in an accident |

| Bodily Injury (per accident) | $60,000 | Total injuries or death to multiple people in the same accident |

| Property Damage (per accident) | $15,000 | Damage you cause to someone else’s car or property |

These limits can still be overwhelmed by modern repair and medical costs. They’re better than older minimums, but they can remain a tight squeeze in real-world crashes. (Always verify your exact limits on your declarations page.)

Why This Is Becoming a Bigger Problem Now

This lesson hits harder today than it did a few years ago. Vehicles are more expensive to repair, parts cost more, and medical care expenses continue to rise. Meanwhile, traffic density and distracted driving risks haven’t exactly improved.

There’s another issue many people overlook: if you’re hit by someone with low coverage—or no coverage—your own policy suddenly matters far more than expected. That’s where options like uninsured/underinsured motorist protection can make a meaningful difference depending on your situation and budget.

As a result, the question many drivers are asking has shifted from: “What’s the cheapest policy I can get?” to: “What happens to me if something actually goes wrong?”

The Illusion of “Cheap” Insurance

Low monthly payments feel great, especially when rent, groceries, and gas all cost more than they used to. But cheap insurance only saves money in one scenario: nothing ever happens.

As soon as there’s a crash, coverage gaps appear quickly. Low liability limits, missing protections, and exclusions you assumed were included can leave you financially exposed. The trade-off behind a “great price” is often a policy that doesn’t provide meaningful protection when you need it most.

This doesn’t mean everyone needs the most expensive policy available. It means understanding what you’re giving up in exchange for saving a few dollars each month.

Why Comparing Policies Matters More Than Ever

Many drivers don’t realize that two people with similar driving histories can receive very different quotes from different insurers. Each company evaluates risk differently, and pricing can vary significantly—even when coverage appears similar at first glance.

That’s why comparison shopping matters. The goal isn’t just finding the lowest number—it’s finding the right balance between affordability and real protection. In many cases, slightly higher limits don’t always translate into dramatically higher premiums.

- Check liability limits first (this is your financial “ceiling”).

- Look for protection against uninsured/underinsured drivers if it fits your situation.

- Compare deductibles and exclusions—not just the monthly cost.

- Ask what factors impact your premium the most.

The Confusion Around “No Down Payment” and Payment Flexibility

Another trend gaining attention in California is “no down payment” or “low upfront” insurance. For drivers under financial pressure, the idea of starting coverage without a large initial bill is understandably appealing.

However, this phrase is often misunderstood. In many cases, it reflects how the first payment is structured—not that the insurance costs less overall. Monthly premiums may be higher later, and certain billing arrangements can include additional fees.

If you’re exploring flexible billing, it’s important to understand how buy now, pay later car insurance options typically work, so you can distinguish between marketing language and the actual payment structure.

Most importantly, payment structure does not change your coverage limits. Low limits remain low limits, regardless of how the premium is divided.

What Drivers Should Do Instead

The solution isn’t panic-buying maximum coverage. It’s slowing down and asking better questions before committing:

- If I cause an accident, how much could it realistically cost?

- Could I afford the difference if my coverage runs out?

- What happens if the other driver has little or no insurance?

For many drivers, modestly increasing liability limits and considering uninsured/underinsured protection can significantly reduce worst-case financial risk without dramatically increasing costs. If budget is a concern, ask insurers to compare minimum limits with slightly higher options—you may be surprised by the difference.

The Takeaway

California drivers are learning—sometimes the hard way—that minimum coverage isn’t the same as meaningful protection. Insurance isn’t only about legality or price. It’s about what happens on your worst day, not your best one.

Taking the time to compare quotes, understand coverage limits, and look beyond the monthly payment can help prevent long-term financial stress later. It’s a lesson worth learning before an accident forces it on you.

FAQ

Is minimum coverage illegal if it meets state requirements?

No. If your policy meets California’s minimum requirements, it satisfies the legal baseline. The issue is that “legal” doesn’t always mean “financially sufficient” in a serious accident.

Do higher limits always mean much higher premiums?

Not necessarily. The increase from minimum limits to the next level is often smaller than expected, depending on your profile and insurer.

What’s the biggest mistake drivers make when shopping?

Focusing only on the monthly price. Two policies can appear equally affordable while offering very different levels of protection.

Does “no down payment” mean the policy costs less?

Usually not. It typically refers to how payments are structured, not the total cost. Always review the full payment breakdown and any associated fees.